It’s frustrating. Stock markets in developed economies are tanking, and as a result …

Investors are spooked,

and passing up top-performing,

high-quality businesses in Africa

— Earnings growth of over 50%

— Low valuation multiples

— Paying double-digit dividends

- Tim Staermose

It’s really no secret that my secret sauce in making large gains in investing is to buy low. But when the chips are down and despair has set in, it’s difficult for most people to go against the prevailing market psychology.

Even non-investors would have heard it’s been a sea of red for stock markets almost everywhere this year. The S&P500, one of the “safest” long-term investments is down by double digits. On 13 September the NASDAQ index in the USA sold off by more than 5% in a single session. People are scared.

The sell-off was probably long overdue. The S&P500 had a great run from 735 in 2009 to almost 4,800 at the beginning of this year. But no tree grows to the sky, and it took rapidly rising inflation rates, and concomitant central bank policy interest rate hikes to burst the bubble.

This has had a ripple effect on other major markets in Europe, Asia and even Africa. Also not helping has been high commodity prices and elevated transportation and logistics costs thanks to the high oil price, exacerbated by the Russian invasion of Ukraine.

Investor psychology is such that people often get defensive and adopt a wait-and-see attitude when markets generally look shaky and vulnerable to the downside. That’s certainly been the case for the bulk of this year, but a buyers’ strike only became noticeable at the fund I manage from July onwards.

However, I remain convinced there’s no better time to invest in the frontier markets than now. Many of the biggest and best companies where I invest—thousands of miles away from Wall Street and the City of London— are still performing extremely well, and they’re selling for what I believe will prove bargain prices in the long run. You just need to have the courage to buy them!

Financial results for first half 2022 show our biggest investments

enjoyed earnings growth of as much as 53.5%

The investment fund I started in late 2020 is focused on blue-chip companies in the frontier markets of Sub-Saharan Africa. While I’m normally based in Tanzania, where about half the fund’s capital is deployed, this week I’m in Lagos, Nigeria looking for new investment opportunities here.

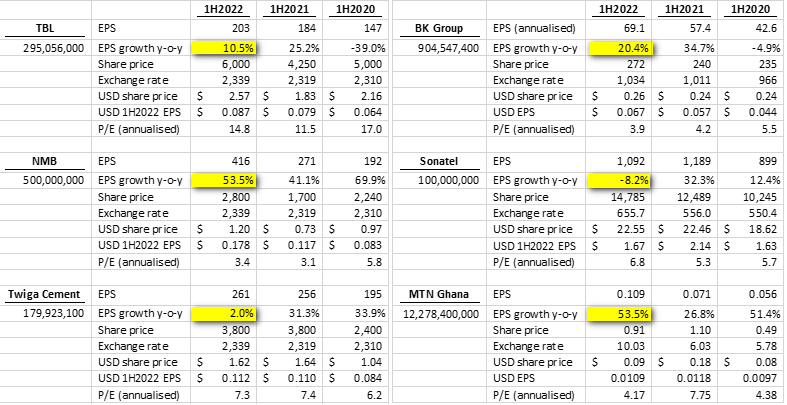

Below is a table of our six largest holdings, which together account for nearly two-thirds of the African Lions Fund portfolio (65%). You will see that for five of them, earnings per share (EPS) growth has been extremely healthy for the first half of 2022.

The one exception, Sonatel, saw its EPS is decline 8.2%. That’s because a large share of earnings went to minority interests this year. That was not the case for the same accounting period last year and may have been due to a timing difference. That said, I still expect Sonatel’s full-year profits to be up by double digits.

For NMB Bank (one of the top two banks in Tanzania) and MTN Ghana (largest mobile phone operator in Ghana), 1H2022 EPS growth both came in at a whopping 53.5%.

You may have noticed that the 53.5% growth for MTN Ghana is negligible in USD terms. That’s due to the Ghana Cedi declining sharply versus the strong US dollar. But for our other stocks, the USD EPS figures, and USD share prices, are holding up, even in the face of amazing USD strength.

I have annualized the numbers in the table for simplicity in most cases, but you can also see that there has been little or no valuation multiple expansion. Most of these stocks are cheaper now on a P/E multiple basis than when we first began to invest in the fourth quarter of 2020. Only Sonatel and Twiga Cement have seen slight multiple expansions.

NMB in particular stands out. EPS has more than doubled from 192 for the first six months of 2020 to 416 for the first half of 2022. My estimate is that the bank will end up making 850-900 for the full year 2022. As such, the P/E multiple which was 5.8x in 2020 is just 3.4x now. In my book, that’s a “steal”.

Bottom line: nearly all of our portfolio’s appreciation thus far has been driven by earnings growth and not by valuations becoming more expensive.

Let’s use the formula:

P = P/E * E

… where P is the price of the stock, P/E is the ratio of price over earnings per share, and E is the company’s earnings. There are several different ways for the stock price to appreciate:

- P/E can rise, and E can stay the same.

- P/E can rise and even if E falls, if the rise in P/E is big enough, share prices can go up.

- This is an indication that the stock may be overvalued and is what we’ve seen during the dot-com boom and the rise of the unicorns

- P/E can fall, and E can rise by more than enough to offset the P/E decline

- This is the current situation we have in the frontier African stocks that African Lions Fund owns. It indicates that the stocks are most likely undervalued, hence representing bargains.

- P/E can rise, and E can also rise

- This is what we are hoping will happen, as more investors gain confidence that the remarkable earnings growth of the stocks we own can continue, and they then begin to bid them up.

Based on these criteria, hopefully we have the effect of valuation multiple expansion and the resultant price kicker still to come.

Meanwhile, regardless of what’s going on in stock markets…

The managements of the companies we own

are working diligently to maximize stakeholder value

During August I had the opportunity to attend the Tanzania Breweries Limited (TBL) AGM and meet the CEO and CFO at the company’s Dar es Salaam head office the following day. After that meeting, I also toured the Dar es Salaam brewery, one of four that the company owns and operates around the country. The others are in Mbeya, Moshi, and Mwanza.

These cities may not mean much to you, if you’ve never been to this part of the world, but they’re important as they house the best breweries in the whole of Africa. Along with Dar es Salaam, ranked number 2, Mbeya, ranked number 1, Mwanza number 4 and Moshi number 5, TBL is on top of its game having four of the top five breweries in Africa ranked for efficiency.

It’s testament to the high quality of this company’s operations. From what management conveyed, they are confident that 2022 results should match or exceed their bullish forecasts.

At Twiga Cement, where I last met with CEO Alfonso Velez in mid-July, 2022 has also been a good year so far. After a recent price hike for its entire product range, Twiga should be able to grow EPS at a faster pace in the second half than it did in 1H2022.

Overall, after two back-to-back massive years in 2020 and 2021, earnings growth and dividend payout are expected to be more muted this year. The company plans to retain more of its earnings to reinvest in capacity expansion, but still maintain the dividend at TZS 390 per share.

We have already collected some very handsome dividend payouts

The level of dividends the African Lions Fund portfolio earns is substantial, and really helps serve as a bulwark for our performance during periods of great market volatility such as that we’ve experienced in recent months.

Seven of our stocks trade on historical yields in double digits:

- 12.2% (Kenya)

- 11.9% and 14.7% (Ghana)

- 16% and 10.1% (Tanzania)

- 10.3% and 10.6% (Rwanda)

We have three other stocks on yields in the high single digits, in Uganda, Tanzania, and Senegal.

In some cases, with very high payout ratios, we’re reinvesting our dividends to get the benefits of compounding over the long run.

Indeed, there are some modest dividend payments coming from BAT Kenya and Safaricom, and I will be looking to reinvest these in the Kenyan market.

This is one of the truly great things about investing in high-quality businesses here in frontier African markets. Even when many stocks and market indices here, and around the world, are under significant selling pressure, as they have been lately, the dividends roll in.

Investments made by African Lions Fund were

largely insulated from declines in Africa’s big economic powerhouses

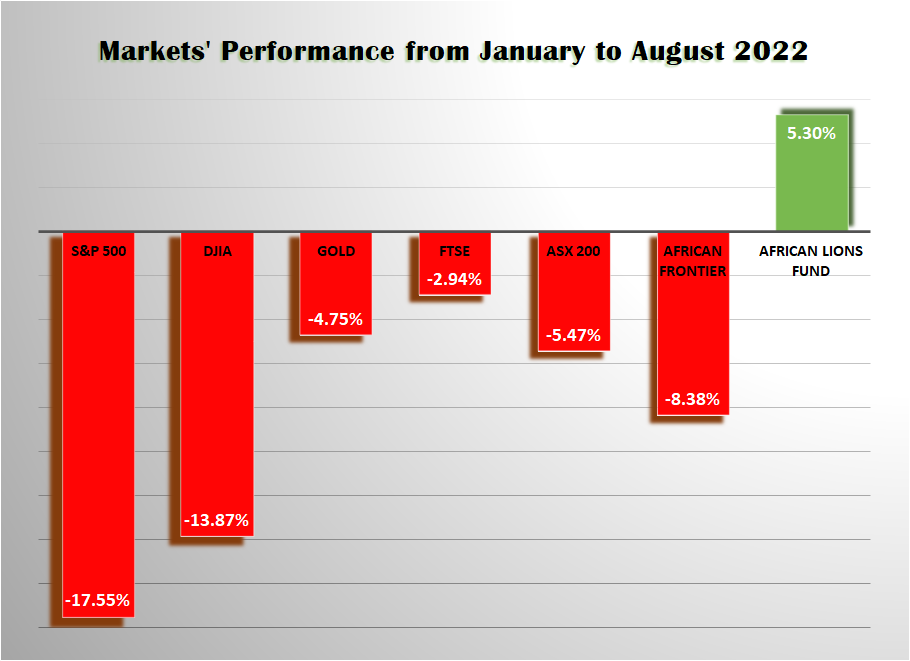

In African frontier markets, the index I use as the performance fee hurdle for my African Lions Fund is also down 8.38% this year. That’s because it has a significant weighting to Nigeria and Kenya, two African economic powerhouses, but with pressing political and financial problems at present.

Kenya just finished its Presidential election, William Ruto was declared the winner by a margin of less than one percent, which the opposition candidate Raila Odinga disputed. But following due process, the Supreme Court upheld the result.

A peaceful transition of power that followed the constitutional process to the letter is to be commended. But President Ruto faces many pressing problems, including food scarcity in the drought-affected parts of Kenya, high levels of public debt, a scarcity of US dollars pushing the exchange rate to all-time lows versus the dollar, high unemployment, and pervasive corruption.

Meanwhile, in Nigeria—home to Africa’s largest population and wealthiest businessman, Aliko Dangote—the presidential election is about 6 months away. And there is a long-running foreign exchange crisis. People have been trying to dump their Naira in exchange for anything they can get their hands on, including dollars, gold, real estate, and more recently stocks.

Recently, I have been putting some money into Nigeria, using dual-listed Nigerian shares that trade in London. When you transfer the shares to Nigeria and sell them there, it’s possible to end up with more than twice as much money in Nigerian currency than you would get by simply wiring cash to Nigeria and exchanging it at the official exchange rate.

With some dry powder sitting in Nigeria, I want to be ready to invest, should things start looking up, for example, after the Presidential election. That’s why, right now, I’m Nigeria for a week of company meetings to see what I can learn on ground.

Overall, African Lions Fund is standing strong:

up 5.3% year to date, and gaining 38.7% since inception

As evidenced by their results, the companies that we have the largest amounts of our capital invested in at African Lions Fund are doing fantastically well, and they will almost certainly be doing even better over the months to come.

I’m not expecting any, but if there were to be significant dips in the share price of companies we own, far from worrying about having invested at higher levels, and not timing the exact bottom (no one can), I’ll be gleefully taking advantage of such dips to buy more shares.

The problem is new capital has been hard to come by. Recently, I had to reallocate capital from one of our more fully valued investments in Mauritius, in order to put the capital from there to work in even better opportunities. Moreover…

I’m putting my money where my mouth is:

I’ve (re)invested my fees from the fund this year

These are the accrued performance fees that are likely to crystalize and be owing to me at year end, which we had been keeping aside in cash until they are normally allocated, in January.

Most likely I will leave this money in the Fund anyway come January, but as I’m seeing good investments now, left and right, at attractive prices, I decided to put it to work early for the benefit of everyone in the fund. It is a modest amount in the big scheme of things (just over 1% of the entire Fund), but when one can buy shares in the likes of Tanzania Cigarette Company on a multiple of 8 times indicative earnings, and a dividend yield of 16%, it behooves one to take the opportunity presented.

For whatever reason, this was an opportunity that came up during August, and I duly pounced on it. We also just bought more Twiga Cement. And we’re adding to our position in the most profitable listed company in Rwanda.

I am also adding to our positions in Kenya at present, including one new investment there.

My outlook for the stock market as a whole

My opinion on that is that with the energy crisis hitting Europe, cost of living increases and interest rate hikes, the earnings of many developed market stocks are about to take a BIG hit.

Let’s use our formula again:

P = P/E * E.

If E goes down, P/E needs to go up (a lot) for share prices to rise. Does that seem realistic when interest rates are also rising?

More likely, P/Es contract, E also falls, and P takes another lurch down. But I don’t know. All I know is that what I have been buying for my investors in Africa makes a lot of sense, regardless of what happens to the S&P 500 and other developed market indices.

Given the offers of blocks of shares for sale in the markets where I invest, I could easily put several million dollars more to work quite quickly in excellent businesses that we already own.

However, with little new capital being contributed, it is, somewhat frustratingly, not possible to take all the opportunities I am being presented with right now.

If you, or someone you know, is looking for a good investing opportunity right now, you might just find it on my side of the world. I am doing exactly what I set out to do: “Pick the best low-hanging fruit where few others look — for cents on the dollar.”

As stated, the Fund remains up 5.3% as of 31 August 2022. It’s outperforming the S&P 500 by over 20%.

It’s always more fun to have more investors along for the profits, and with my +38.7% performance over the first 23 months of the fund’s existence, I’m actually walking the walk, and delivering the aimed-for compound returns that could see our investments double every 5 years, ideally.

If it makes sense for you, I hope you will consider joining me.

Until next time,

Good Investing!

![]()

Tim Staermose

Founder, Global Value Hunter

& African Lions Fund Ltd.